What is a Roth IRA?

Not all Individual Retirement Accounts (IRAs) were created equal.

There are a number of different types of IRAs: Traditional, SEP, SIMPLE, Self-Directed, and Roth. While there are some differences in their eligibility rules and contribution limits, all but one offer the same tax benefits.

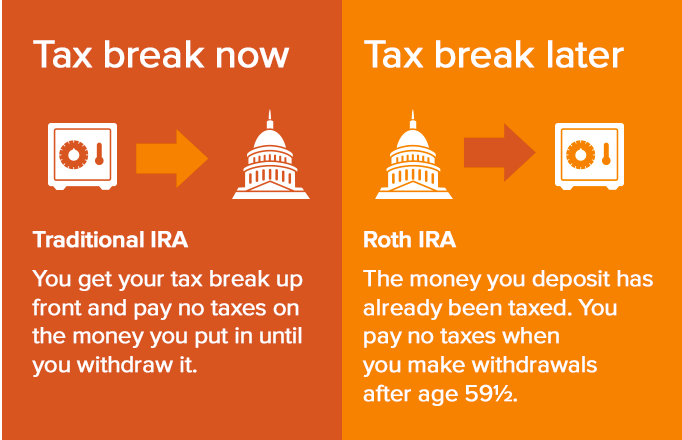

That is, contributions to an IRA are tax deductible and interest earned on the contributions is not taxed until it’s withdrawn.

The exception is the Roth IRA.

The tax benefit of a Roth IRA is substantially different than all other IRAs in that contributions to a Roth IRA are not tax deductible. In addition, contributions as well as the interest earned within the Roth IRA are not taxed upon withdrawal.

Basically the Roth IRA gives you a tax benefit in retirement, while all other IRAs give you most of your tax benefit at the time of your contribution.

Let’s look at an example. Sabrina Lopez is single, earns $40,000 a year and is in the 25% tax bracket. If she contributes $5,000 to any IRA except a Roth IRA, she will lower her taxable income by $5,000 and will save $1,250 in taxes ($5,000 x 25% = $1,250). However, if she contributes $5,000 to a Roth IRA she will not save $1,250 in taxes because you can't deduct a Roth IRA contribution.

Let’s say that she contributes $5,000 a year to an IRA for 20 years ($5,000 x 20 years = $100,000). Over that time, let's say she earns $45,000 of interest. If she contributed to any IRA, except a Roth IRA she would owe taxes on the $100,000 of contributions as well as the $45,000 when it is withdrawn, after she reaches age 59 ½.If she contributed to a Roth IRA, she would not owe any taxes on the $100,000 of contributions and $45,000 of interest when it is withdrawn. In effect, she is giving up $1,250 in tax savings each year to avoid paying taxes on the $45,000 of interest in retirement.

Which IRA will give Sabrina the best tax benefit? As a general rule, the answer is the Roth IRA.

This is because with all IRAs, other than the Roth IRA, you must pay tax on the interest earned. There are scenarios where you could end up with more money if you invest with any IRA other than a Roth IRA, but these scenarios assume you will be in a lower tax bracket when you retire.

However, it’s impossible to predict what the tax rates will be for you during your years in retirement. Therefore, I don’t recommend basing your decision on which IRA to choose on future tax rates.You can find a variety of calculators on the Internet that will compare the relative tax benefits of a Roth IRA and all other IRAs. A good one can be found here.

In addition to these tax benefits, there are other advantages to a Roth IRA over other IRAs:

You can withdraw your Roth IRA contributions tax-free at any time, even before you reach age 59½. Withdrawals of contributions from all other IRAs before age 59½ will result in a 10% penalty, as well as taxes owed.

You can withdraw the earnings on your Roth IRA contributions tax-free after you reach age 59½, as long as you have held them within the Roth IRA for at least five years, beginning with the first taxable year the contribution was made. If you withdraw earnings from your Roth IRA before reaching age 59½, you may owe taxes and penalties on your withdrawals. Withdrawals of earnings from all other IRAs are always taxable.

All other IRAs require that you start withdrawing your money after reaching age 70½. Not so for the Roth IRA. The Roth IRA allows you to continue to earn interest tax-free for as long as you want. If you decide to give your Roth IRA to family members in your will, they can avoid paying taxes on it as well.

Roth IRA 2022 Contribution Limits

The maximum you can contribute to a Roth IRA is the same as a Traditional IRA - $6,000 per year. If you are age 50 or older, you can contribute up to $7,000.

Roth IRA 2021 Eligibility Rules

If you file as married filing jointly (or a qualifying widow(er)), you can contribute the maximum amount if your modified adjusted gross income is less than $204,000.If you file as single you can contribute the maximum amount if your modified adjusted gross income is less than $129,000.If you file as married filing separately and you lived with your spouse at any time during the year, you can contribute the maximum amount if you have no modified adjusted gross income.If you meet the above eligibility rules, you can contribute to a Roth IRA even if you or your spouse participates in a qualified retirement plan, such as a 401(k).

Closing

If you haven’t thought about a Roth IRA before now, it’s to your advantage to do so. Each year you wait before deciding to contribute to a Roth IRA, you will have less money in your retirement. With the tax and other benefits of a Roth IRA, it’s well worth it!See also my article: "How a Roth IRA Can Benefit Your Dependents."

Tom Copeland - www.tomcopelandblog.comImage https://www.voya.com/article/iras-traditional-and-roth

For more information about Roth IRAs and other IRAs, see my book Family Child Care Money Management & Retirement Guide.